Cross-Border Crypto Payments: How Stablecoins Are Changing International Money Transfers

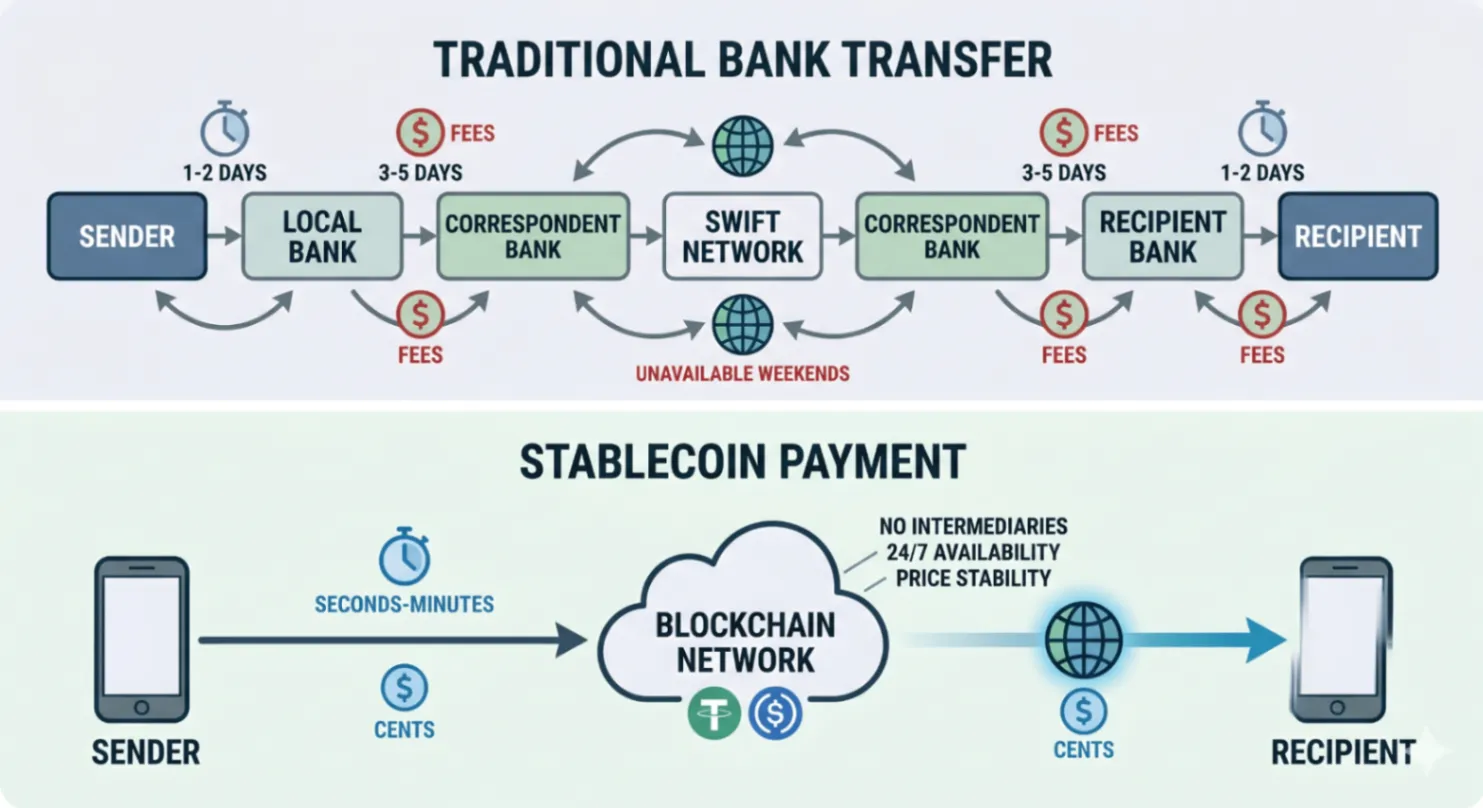

International money transfers are slow, expensive, and unnecessarily complex. A bank wire between countries can take three to five business days, cost a percentage of the total in fees, and involve multiple correspondent banks who each take a cut. For freelancers billing international clients, for migrants sending remittances home, and for businesses paying overseas suppliers, this friction represents a significant and largely avoidable cost.

Cross-border crypto payments — particularly those using stablecoins — offer a fundamentally different model: near-instant settlement, predictable fees, no intermediaries, and 24/7 availability. This article explains how it works and why it matters.

The Problem with Traditional International Transfers

The global banking system was not designed for the internet age. SWIFT, the messaging network that underpins most international bank transfers, was established in 1973. The correspondent banking system requires multiple banks to cooperate to move funds between countries, each adding time and cost.

The practical result:

- A SEPA transfer within Europe typically settles in one business day — but international transfers outside SEPA can take 3 to 5 business days

- Fees typically range from 2% to 5% of the transferred amount, or flat fees that are disproportionately costly for small transfers

- Exchange rate markups add further hidden costs when currencies must be converted

- Transfers can be blocked, delayed, or reversed by banks at various points in the chain

- Transfers are unavailable on weekends and public holidays

How Crypto Changes the Equation

A cryptocurrency transfer is a message on a blockchain network that permanently records the movement of value from one address to another. There are no correspondent banks. There is no SWIFT network. There is no business hours restriction. The sender and recipient interact directly with the blockchain, and the transaction completes when it is confirmed by the network.

Transfer time:

- Bitcoin: approximately 10 to 60 minutes for full confirmation

- Ethereum: seconds to minutes depending on network congestion

- BNB Chain, Polygon, and similar: typically seconds

Transfer fees:

- Blockchain network fees (gas) that are independent of the amount being transferred — sending $50,000 may cost the same as sending $50 on the same network

- No intermediary fees, no correspondent bank markups, no currency conversion fees if sending in the same currency

Why Stablecoins Are the Practical Solution for Cross-Border Payments

While Bitcoin and Ethereum are effective for transfers between crypto-native users, their price volatility creates a problem for everyday commercial use. A freelancer who invoices in USDT and receives USDT knows exactly what they will receive, regardless of what Bitcoin's price does between invoice and payment.

Stablecoins — primarily USDT (Tether) and USDC (Circle) — are cryptocurrencies pegged to fiat currencies, typically the US dollar, at a 1:1 ratio. They combine the settlement efficiency of blockchain technology with the price stability of fiat currency.

The practical result: a payment from a client in Germany to a freelancer in the Philippines can be sent in USDT and received within seconds, at a cost of cents, with no exchange rate risk on the crypto leg of the transaction.

Who Benefits Most from Cross-Border Crypto Payments?

Freelancers and Remote Workers

The global freelance economy has grown substantially, with platforms creating payment flows across dozens of currency pairs. Cross-border crypto payments allow freelancers to receive payment immediately and with minimal fees, regardless of where their clients are located.

Migrant Workers and Remittance Senders

Remittances represent one of the largest financial flows in the global economy — hundreds of billions of dollars sent annually from workers in wealthier countries to families in developing economies. Traditional remittance services can charge 5% to 10% on small transfers. Crypto stablecoins can reduce this to less than 1%, with near-instant settlement.

Small Businesses with International Suppliers

Businesses paying overseas suppliers face the same delays and fees as individuals, compounded at scale. Crypto payments can streamline accounts payable for international transactions, improving cash flow and reducing cost.

Using a Stablecoin Payment App: How It Works in Practice

- Both parties need a crypto wallet that supports the relevant stablecoin (USDT or USDC)

- The sender requests the recipient's wallet address on the chosen network

- The sender initiates a transfer of the agreed amount in stablecoins

- The recipient receives the funds, typically within seconds to minutes

- The recipient can hold the stablecoins, swap them for other crypto, or convert to local currency

DokWallet supports USDT and USDC across multiple networks, making it an effective tool for cross-border stablecoin payments. The ability to choose the network (Ethereum, BNB Chain, Polygon) allows users to optimise between transaction speed and cost.

Important Considerations

Cross-border crypto payments are not without complexity:

- Both parties must have compatible wallets and addresses on the same network — sending USDT on Ethereum to a BNB Chain address would result in lost funds

- Tax treatment of stablecoin receipts varies by jurisdiction — freelancers should consult a local tax advisor

- Recipients who need local currency must have a path to convert — this varies in accessibility by country

- Stablecoins carry their own risks, including issuer risk — USDC is generally considered more transparent than USDT

Conclusion

Cross-border crypto payments using stablecoins represent one of the most compelling practical applications of blockchain technology. For anyone who regularly sends or receives money internationally — whether as a freelancer, a remittance sender, or a business — the cost and speed advantages over traditional banking are substantial and immediate.

The technology is accessible today, through apps like DokWallet, and the learning curve is modest. For those paying or receiving hundreds or thousands of dollars in international transfers, even modest adoption of stablecoin payments translates to meaningful savings.